If you’re struggling with credit card debt, you’re not alone! According to CNBC, “Nearly half (47%) of U.S. adults, or about 120 million people, currently have credit card debt.” I guess you could say credit card debt is pretty normal. But we don’t want to be normal. We want to be free of credit card debt so we can live financially amazing lives! Let’s go over 10 tips that are game-changers for paying off credit card debt fast.

I know these tips will work for you because many of them worked for me! When we were on our own journey to pay off $71k of debt in less than 3 years, we had around $3,200 of credit card debt to pay off. And we did it! So I know you can do it too.

With higher and higher interest rates and predatory contractual agreements, getting out of credit card debt is on millions of people’s wish list, but it doesn’t just have to be a wish– it can be your reality.

If this is you, here are my top 10 tips for paying off your credit card debt.

10 Tips for Paying Off Credit Card Debt Fast

1. Get on a Zero-Based Budget

The first and most important piece of advice for paying off credit card debt is to get on a Zero-Based Budget. I know, I know– this isn’t the most earth-shattering or fun piece of advice, but getting on a budget, specifically a Zero-Based Budget, can be life changing. I’m speaking directly from my life experience.

When my husband had his first corporate job, we got a credit card to help us relocate. We continued using it monthly and paying it off until November 2016. My husband made a huge purchase on the credit card that we couldn’t afford to pay off that month. I hated feeling like we were living outside of our means. Our credit card debt was the straw that broke the camel’s back. I realized that we were spending over $1,300 per month on just minimum payments to our debt.

A Zero-Based budget is what saved my family’s finances. I created my first Zero-Based Budget to pay off the $3,200 in credit card debt we had accrued. After the credit card debt was paid off, we used this method of budgeting to pay off an additional $68,000 and become debt-free.

So, while it may not be a thrilling tip to pay off your credit card debt using a Zero-Based Budget, it is a powerful and necessary one.

2. Focus on one debt at a time

In addition to getting my family on a Zero-Based Budget, we decided that in order to pay off our credit card debt, we needed to put all of our focus on one debt at a time.

There are multiple methods of paying off debt, and I would say that no one method is “the best method”. It all depends on where you are in life and what will work best for you and your family. However, I can say with absolute certainty that The Debt Snowball Method has worked for my family and millions of others in the same debt boat as we were.

I particularly like The Debt Snowball or The Debt Avalanche Method because it forces you to tackle one debt at a time. This takes away the overwhelming feeling you would have if you looked at all of your debt at once. Trust me, if I had tried to tackle multiple debts at the same time and considered all $71,000 at once, I wouldn’t have paid it off. It would seem completely impossible and unattainable. With The Debt Snowball Method, I could focus on the $3,200 worth of credit card debt first, instead of the $71,000 in debt total. Just that sharp focus made all of the difference on our debt-free journey.

3. Save up an emergency fund

The average American can’t take on a $400 emergency without going into debt. That’s why having an emergency fund is absolutely crucial when you are paying off debt, and especially when you are focusing on credit card debt. What’s the point of paying off thousands of dollars if you just swipe your credit card when your tire blows because you don’t have any cash on hand?

An emergency fund will help you stay out of debt and prevent taking on new debt!

This step is actually more difficult than I think many people will admit. Why? Well, when you decide that you want to pay off debt, you want to start right now. Trust me when I say you need to slow your roll and build up an emergency fund first.

Ready to save up? Use the Easy Budget FREE Savings Tracker HERE

Life will happen, unexpected events will occur and, yes, you’ll have to pay for something you didn’t foresee — but, that’s okay, because when you have an emergency fund an emergency tends to become a simple inconvenience. Having an emergency fund ensures that you won’t go back into debt and allows you to focus on fixing the problem instead of ruminating on how much the said problem is going to cost you later down the line.

Imagine not having to worry about money regardless of the situation you were put in? That’s the true power of an emergency fund.

4. Physically cut up your credit cards

You know what keeps you from swiping your plastic over and over again? Cutting your cards up. I know that some of you read that and are now clutching your wallets or purses, screaming “Over my dead body, Merilee!” I would be lying to you if I said I didn’t get that reaction, because I truly do, but I also promise you that this tactic will expedite your credit card debt payoff.

Once you are on a Zero-Based Budget and you’ve saved an emergency fund to fit your lifestyle, I recommend physically cutting up your credit cards. Cutting up your credit cards is like a personal declaration that you’re all in this. There’s no turning back when those bits of plastic are sprawled across your kitchen counter. You’re putting the nail in the credit card debt coffin, so to speak.

I encourage you to go through this credit card cutting “ritual,” but I also want to remind you that not having credit cards doesn’t have to be forever. While you’re working through your credit card debt and unlearning toxic financial habits, not having the credit cards around will help you not revert back to swiping them constantly or using them for an emergency in lieu of cash on hand.

Once you have a handle on your personal finances, credit cards are just another tool to use if you are able to control them.

5. Try a 0% APR transfer

If you’re ready to pay off your credit card debt, but you’re being buried by the high interest rate each month (like 20-25%+), I recommend considering a 0% APR credit card transfer.

Many, if not all, credit card companies offer some sort of 0% introductory APR rate credit card. Companies do this to entice people to switch to their credit card and reap credit card rewards at a 0% interest rate for a set amount of time, hoping that the 0% transfer card customer will become a permanent one.

This tactic has turned out to be quite the credit card debt payoff loophole, as people have started transferring their high credit card debts to 0% APR cards and paying off their balances without being crushed by high monthly interest rates.

Typically cards have the 0% introductory interest rate for a limited time– typically around 6-18 months. After that period, the 0% APR turns into the contractual interest rate of the card (a national average that hovers around 18%). So after you make a balance transfer, try really hard to pay the card off before that interest sets in! Some of these cards also have transfer fees associated with them, so be aware and do your research.

If you have the financial ability to pay off your credit card debt within that strict time frame, transferring may be the right option for you.

6. Opt for store debit cards instead of store credit cards

Nothing irks me more than when an innocent store associate asks the dreaded question, “Would you like to save 20% on today’s purchase by signing up for our store credit card?” I mean, I completely understand, that’s their job. But ugh! I wish retailers weren’t so eager to make money off of their insane store credit card interest rates!

I know that many people have been sucked in to predatory and exploitive store credit cards, but did you know that there is a work around?

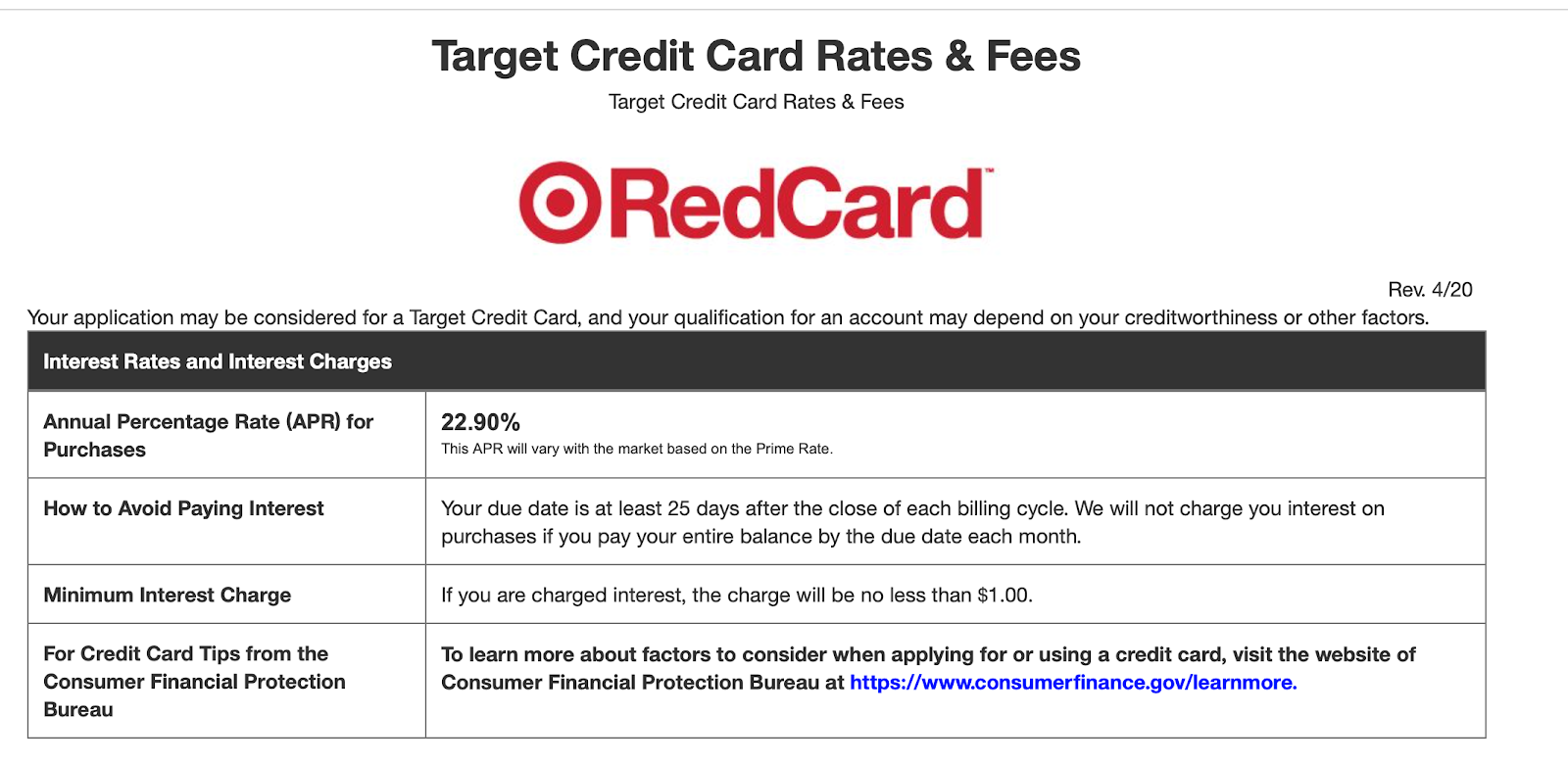

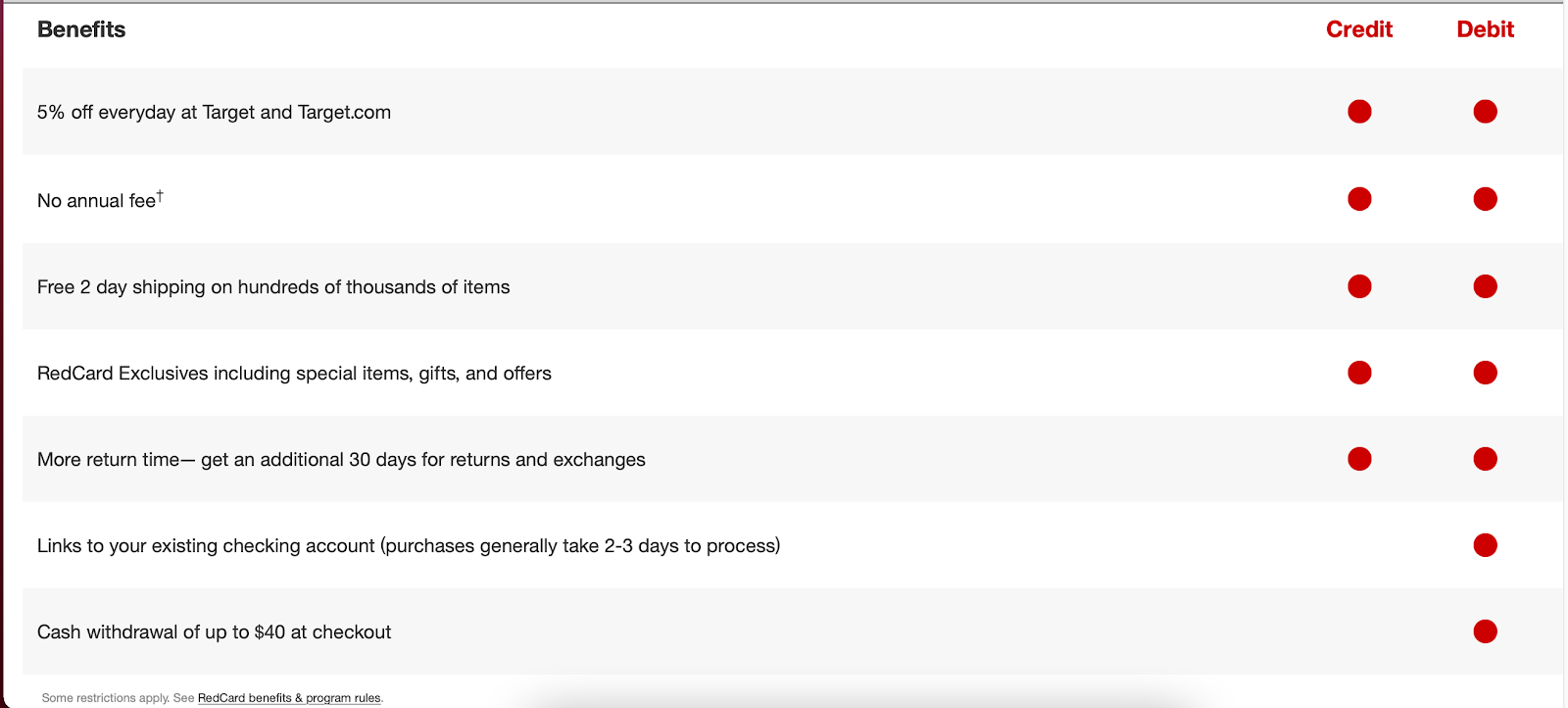

Instead of charging purchases to a retail credit card with a high interest rate, use a store debit card instead. For example, instead of the Target RedCard™ credit card, which has an interest rate of almost 23%, apply for the Target Red debit card that has no interest rate.

The Target RedCard™ debit card actually comes with more perks than their Target RedCard™ credit card, including the same 5% discount.

If you’re looking for a store discount, you don’t have to sign up for a credit card immediately. Dig in to the company and see if they offer a debit card instead of a credit card.

7. Ask for a lower interest rate

Everything in life is negotiable– everything. Even credit card interest rates. The best thing about being brave enough to ask for a lower interest rate when paying off your credit card debt is that you get one of two answers: Yes or no. And if you were too afraid to ask? The answer is always going to be no.

Before you call to ask for a lower interest rate on your credit card, make sure you do your due diligence. Know your current credit card interest rates and balances due, and have a record of how many times you have made on-time payments. This gives you leverage if simply asking doesn’t do the trick.

If you haven’t made on-time payments, I recommend becoming a customer that does make them on time– this will not only improve your credit score in the long-haul, but it will give you a more powerful position when it comes to lowering your interest rate. A credit card company or bank doesn’t want to lose a customer that they can count on to pay their bills on time.

Lastly, research other credit cards with lower interest rates or a company’s competitors. Don’t be afraid to walk away and close your account with your credit card company. As we have already discussed, there are other 0% APR balance transfer credit cards options out there that you can go to if your current credit card company refuses to lower your interest rate.

8. Personal loan with lower interest rate

If a balance transfer isn’t an option for you for whatever reason, look into taking out a personal loan with a much lower interest rate to pay off your credit card debt. While yes, this is technically “shuffling” debt around, this can save you thousands of dollars in interest if you have high credit card debt and are committed to paying it off.

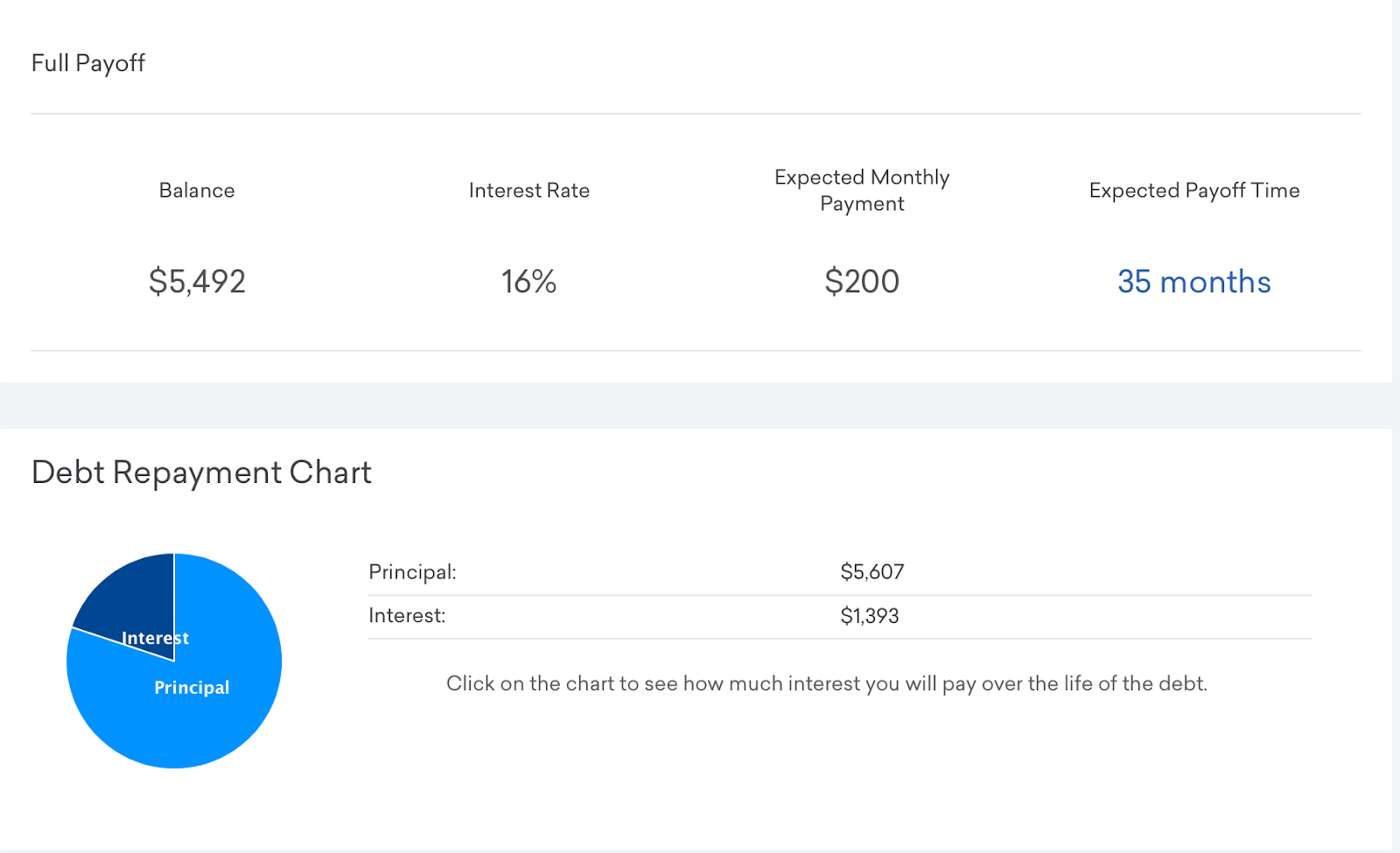

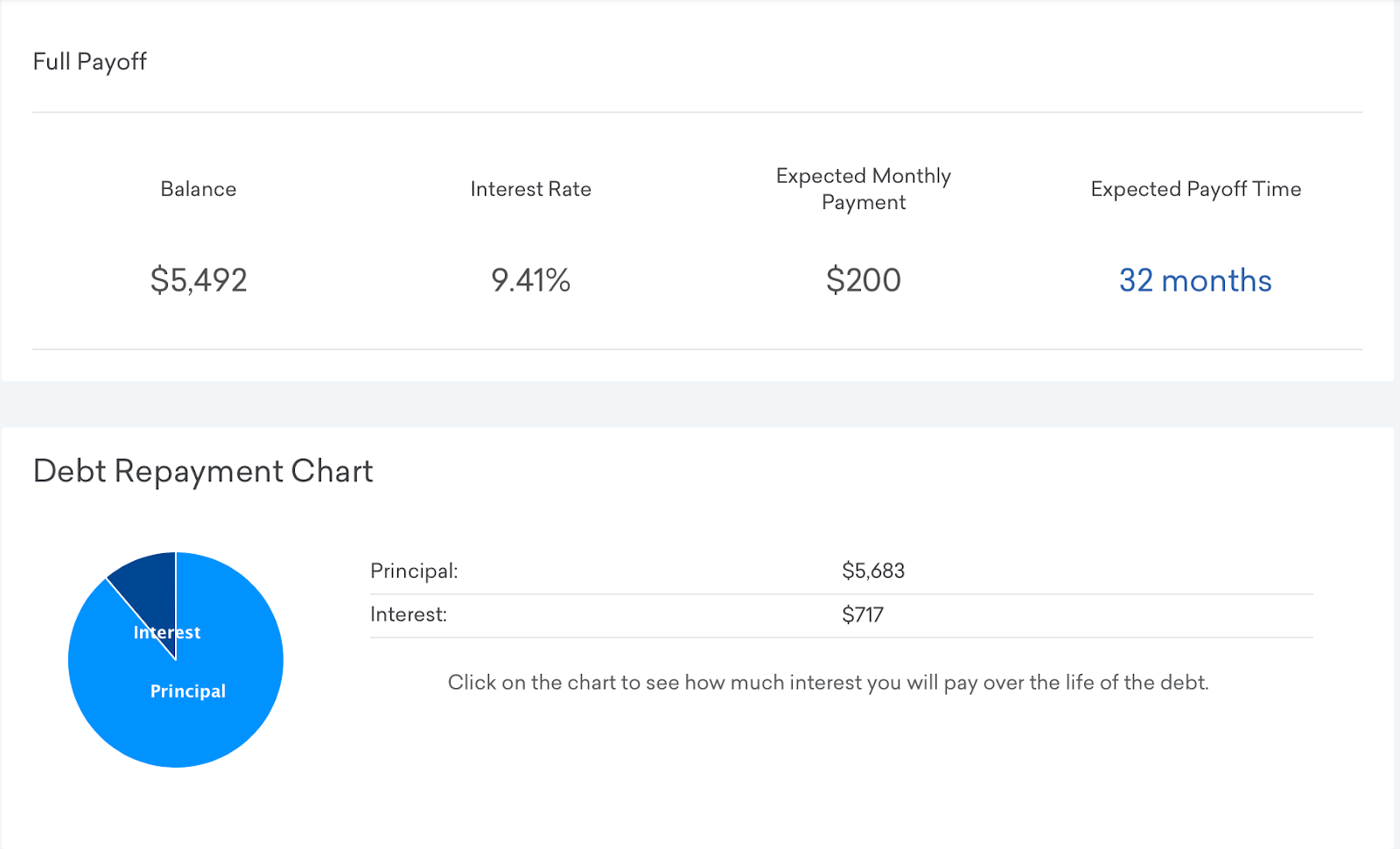

According to Experian, the average interest rate on a personal loan is 9.41% — that’s down 7 points from the average interest rate on credit cards. What does this mean? Let’s compare how long it would take you to pay off $5,492.23 with a monthly payment of $200 via credit card debt with an interest rate of 16% and a personal loan with an interest rate of 9.41%.

By switching to a personal loan, you pay off your credit card debt three months earlier and save over $600 in interest.

9. Side hustle solely for credit card payments

If you have a lower income and are being buried by your credit card debt, it may be time to pick up a side hustle. I write about side hustles often and have an entire list to choose from here, but I want to offer a word of caution: You should not compromise your physical or mental health to pay off your credit card debt early.

Side hustles can be a wonderful way to speed up the debt payoff process– especially if you need to just get high interest rates out of the way to create breathing room in your monthly budget.

I recommend trying out for a side hustle with something that you enjoy. Love animals? Try dog sitting. Are you handy? Try to refurbished furniture and flip it on Facebook Marketplace. Enjoying driving around? Get on Doordash! The possibilities are endless when it comes to making some extra gig money.

Remember to record everything you make, set aside some of it for taxes, and then put the rest toward your credit card debt!

10. Pay your monthly payment every 2 weeks instead of once a month

Using this trick across the board is a great way to come out at the end of the year making an extra payment on all of your loans!

Instead of paying your credit card minimum payment monthly, pay it bi-weekly. If you pay biweekly, or split your monthly bill in half and pay the first half during the beginning of the month and the second half at the end of the month, you will make 26 payments per year. Because there are 52 weeks in a year, this will result in 13 monthly payments — not 12!

This tactic can save you thousands of dollars in interest and reduce the life of your loan, especially if you are focusing on other debt at the moment.

You’ve read through all 10 tips now, do you feel more prepared to tackle your credit card debt? I sure hope so!

With these top 10 tips for paying off your credit card debt, you’ll be well on your way to a credit card-free life!

Did you enjoy this post? Pin it to Pinterest for later!