So you want to start paying off your debt? Such a smart move!

Debt causes you to constantly be paying for your past instead of investing in your future.

Interest payments are often a waste of your hard-earned money, money that could be paying for something amazing you want to have or experience!

When we first decided to tackle our $71,000 of debt aggressively back in 2016, we were paying over $3,500 per year in interest payments!

When I realized how much interest we were paying every year, the gravity of our situation hit me like a ton of bricks. There was no way I was going to keep putting $3,500 per year of my hard-earned money into someone else’s pocket.

I don’t know about you, but I can think of about a thousand things I’d rather spend $3,500 on than interest payments! Suddenly I was very motivated!

Since 2016, we’ve paid off $71,000 of debt as a single income family. We’ve got debt payoff down to a science, and because it’s fairly simple to replicate, I’m going to share how we did it with you so you’ll know how you can do it too!

Related reading: How We Paid Off $71k of Debt in Less Than 3 Years on a Single Income

THE 7 STEPS TO PAYING OFF BIG DEBT

1. Get Motivated

If you don’t really mind the maxed out credit cards or the looming pile of student loan debt, you might not be motivated enough to pay it all off. Paying off debt requires determination and a lot of hard work. You need to be mad at your debt and recognize how it is holding you back from achieving your dreams. You need to know how much interest you are paying every month and how it is stealing from your future. You need to dream about how much better the future will be if you are totally debt-free and are able to use your income for whatever you want, instead of paying off the past!

Make sure you follow me on Instagram where I’m very active and share lots of debt-free motivation!

2. Figure Out How Much Debt You Have

Get out a piece of paper and start writing down all the debts you have. I also have a printable worksheet you can use to guide you. Look up each debtor and then write down every individual loan and today’s balance. If you have a messy debt situation and you don’t even know all your debtors, it’s time to focus. Try to remember, do some research, or even look on your credit report to see if your debtors are listed there. Once you’ve written down every loan you have and today’s balance on it, add up the total. This is your starting point.

When I did this back in 2016 I discovered we had seven debtors, over 22 different loans, and a total balance of almost $71,000. It hurt!

3. Set Up a Budget

I know budgeting is like a curse word. Makes you cringe! This is usually the hardest part for people, but you cannot skip this step! Your budget is the key to your success and you cannot make progress without one.

If you’ve struggled with budgeting in the past, don’t be scared away. We all struggled with budgeting in the past! When it clicks, it will change your life. Budgeting is how you will start to “find” extra money that you will throw at debt to get it all paid off.

When I learned about zero-based budgeting, it finally clicked for me. In the years before, I had just been doing a bit of a spending diary where I wrote down everything we spent at the end of the month and added it up. That won’t work here! To create a zero-based budget, you have to estimate how much money you will make in the upcoming month and plan out every single dollar on paper before the month starts. Every dollar needs a purpose. No dollar goes unbudgeted! Income- expenses = $0. Include any money you’ll put toward debt, savings, or other similar goals as expenses. So to be clear, I’m not telling you to go spend all your money, I’m telling you to plan all your money.

If you want to see A-Z details on how I budget, including a video tutorial with a spreadsheet, click here. It’s too much to write it all in this article! But whatever way you choose to track your budget, you have to figure out a budgeting system that works for you!

Related reading: How to Make a Budget: Step-by-Step Guide + FREE Budgeting Spreadsheet

If you figure out a budget but you don’t have any extra money to throw at debt, it’s time to get creative. Cut back everywhere you can. Sell everything you don’t need, or start a second or third job, side hustle, or something similar. Create extra cash flow however possible to put toward your debt.

4. Decide if You’re Going to do a Debt Snowball, Debt Avalanche, or Something Custom

Once you have a budget and you’ve cut back a little bit or taken on a side hustle to earn a little extra money, it’s time to start throwing extra money at debt as often as possible. There are two main debt payoff methods.

One is the debt snowball method, where you list all your debts smallest to largest and pay the minimums all on debts except the smallest. You’ll throw every extra dollar at the smallest loan until it’s paid off and then move on to the next smallest loan and do the same.

The second is the debt avalanche where you list your debts from highest interest rate to smallest and pay them off in that order.

Depending on your circumstances, you might want to do some kind of custom order. For example, if you have a credit card with a huge interest rate or something similar, you might want to get it out of the way and then use the debt snowball on the rest of your debt.

We used the debt snowball method, and I wholeheartedly recommend it! Even though technically the debt avalanche method will mathematically get you debt-free sooner, I think for the most part it’s more mentally difficult so you’re more likely to pause, quit, or get frustrated. The debt snowball method has you paying off your small debts first so you have some “quick wins.” Those quick wins will keep you going and excited about paying off debt!

5. Estimate How Long It’s Going to Take and Set a Goal

You need to make a plan to pay off your debt and then commit to sticking to your budget and your plan! You can’t go into this with an attitude of let’s see if this works. You are the one who makes it work! You are the secret sauce, my friend!

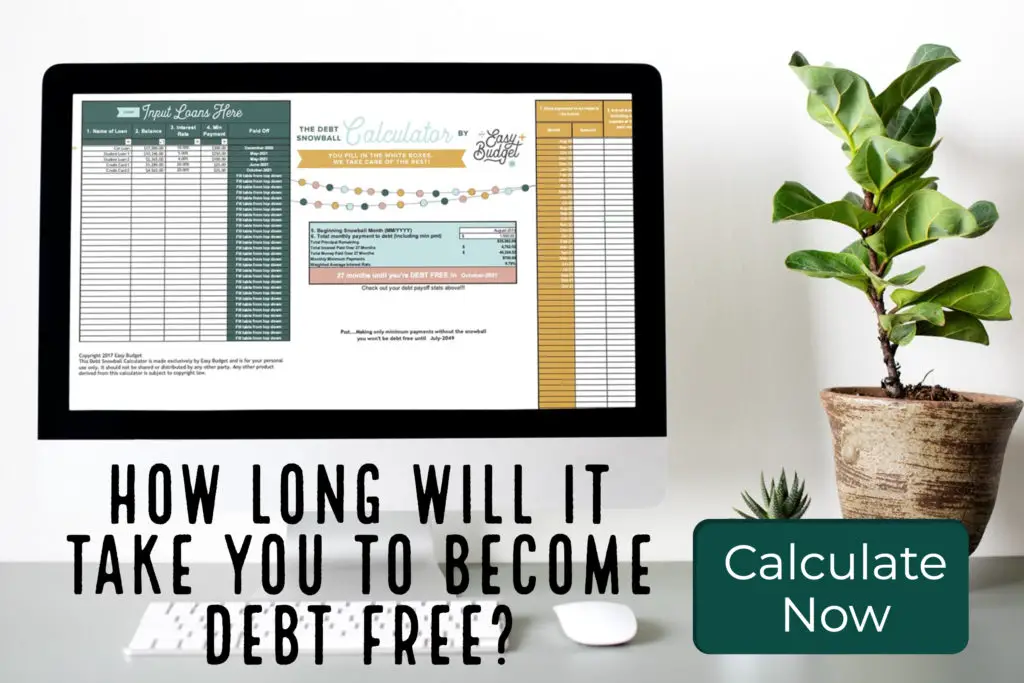

One thing that can make your debt-free goal more clear is knowing how long it’s going to take. We created a Debt Snowball Calculator tool that can help you figure out how soon you can be debt-free based on how much extra you think you can put toward debt every month now and even in the future. This tool will tell you the exact month you’ll be debt-free based on your projections. It’s like setting a “finish line” up for your race!

However, if you don’t mind a rougher estimate, you can guess when you’ll be debt-free based on running a few numbers and go from there.

Make a plan for how much you’ll put toward debt every month and how quickly you can be debt-free with that plan. Set a finish line goal. Don’t worry if things don’t go according to plan every month. They won’t, but you will still make huge progress if you never give up.

6. Get All Responsible Parties on Board

Getting the significant other on board is so important if you want to make real progress, but it’s often a huge hurdle. If your spouse is reluctant, here are a few things you could try:

- Dream out loud with them about all the incredible things you could do in the future if you were financially secure

- Show them how much you pay each year in interest and discuss what you could use that money for instead

- Suggest they read the Total Money Makeover by Dave Ramsey

- Show them how soon you could be debt-free if you put in the work

- Gently bring up the “pain points” of your situation, like the stress or long hours at work

Make sure to be kind and loving, as you don’t want them to feel targeted or undervalued and stop listening to your message.

Be sure you also value their opinion. It’s easy to feel like our way is the right way and that things would be great if they would only listen. But the truth is their opinion matters just as much as yours!

You may need to work a slightly different plan than you were originally thinking, one that takes into account your partner’s preferences, and that’s okay. Do that confidently!

I convinced my husband to read the Total Money Makeover by Dave Ramsey, the same book I had read that got me fired up about paying off debt. Thankfully he likes to read, and got on board. He agreed to let me take the reigns on it. He didn’t stay as motivated as I was throughout the whole journey, though. There were times when he just let me pay off debt but wasn’t really committed or equally on board. I just did the best I could with our situation and kept trying to make forward progress every month.

7. Get Busy and Start Working Your Plan

Sometimes there is no perfect way, you just have to start throwing money at debt every chance you get! It’s time to have some discipline and crack down on bad habits.

I remember paying off our $2,000 car loan on day one. I was so proud! I couldn’t wait to tackle the next debt and feel that weight lifting.

There were times I threw $4000 at debt (like after an exciting work bonus), and there were other times I put $1.29 toward debt! No joke. Every bit counts. Make it a habit of throwing every extra bit toward debt that you can, and magic will slowly start to happen.

There you have it! Following this plan, we paid off $71,000 in about 2 ½ years.

I wholeheartedly believe that you can do this too, even though your numbers and timeline may not match up with mine. I have seen many friends follow this same plan and succeed gloriously. There’s no catch. It’s just hard work that pays off. You can do this too!

Do you need some motivation, inspiration, or a community? Follow me on Instagram where I post inspiration and tips every day!

Did you enjoy this post? Pin it to Pinterest!

One Response

We are working on paying our mortgage off early. We’d like to pay it off with in the next 7 years but can’t calculate when it will be paid off easily. We move next year so we plan to rent it out unsure about what or income/ bills will be at our next location so just trying to stay motivated now and pay off what we can in the present.