Are you ready to take control of your money and turn your financial life around? In this article, I show you how to create a 5 year financial plan that is easy to follow and accomplish!

Why a 5 Year Plan?

It’s the perfect amount of time to change your trajectory toward becoming wealthy! You can accomplish almost all of the major short-term financial goals that will set you up for success in the future.

5 years ago my family was in $71,000 of debt, living on student loans, not using a budget, and clueless about how to get on track financially. Today we are debt-free, we’ve tripled our net worth, we keep a budget, we own 2 income-producing businesses, and we have a long-term plan.

5 years is truly the perfect amount of time to change everything!

I want to help you with your money. I want you to pay off debt, invest, and save. Most importantly, I want you to start where you are right now, because in just 5 years, your life can look completely different if you make a plan and get to work!

Feel free to download my FREE “5 Year Financial Plan” printable to work on as we go along!

Elements That Should be Part of Your 5 Year Financial Plan

Though each of us are different in our circumstances and end goals, a 5 year financial plan will almost always include the following elements:

- Save Starter Emergency Fund of $1,000-$5,000

- Pay Off All Debt (except the mortgage)

- Begin/Increase Investing for Retirement

- Save a Full Emergency Fund (3-12 months of expenses)

- Save for Large Expenses like Downpayment on Home, Vehicle

You will need to decide which order you want to tackle these goals in, and how long each of them will take you. Then you can fit them each into your 5 year plan.

Before you even begin working this plan, you’ll need to learn how to budget. I have dozens of resources on how to budget.

Let’s dive a little deeper.

First, Save a Starter Emergency Fund of $1,000-$5,000

Before you start throwing thousands of dollars at your debt and investments, you need to save a small emergency fund. This will allow you to pay off debt and invest rapidly without worrying about being short on cash if something unexpected comes up.

A good amount for your starter emergency fund is $1,000-$5,000. This is enough to cover most minor emergencies that will come up with cash, and keep diligently working your financial plan.

This should be the first step in your plan if you don’t currently have any money saved.

Related reading: Should You Keep More Than $1,000 In Your Emergency Fund While Paying Off Debt?

Next, Pay Off All Debt Except the Mortgage

Once you have a small emergency fund saved, you can tackle your debt.

Your debt is most likely costing you thousands of dollars per year in interest. That is thousands of dollars you could be keeping for yourself, investing, or using to take a vacation! Say “no more” to debt and kick it to the curb so you can keep your hard-earned money!

First, add up all your debt and figure out how long it will take you to pay it all off. You don’t need to include your mortgage in your 5 year financial plan, but do include all other debts, such as:

- Personal Loans

- Credit Cards

- Retail Credit Cards

- Car Loans

- Cell Phone Loans (yes, this is debt)

- Student Loans

- Medical Debt

- Family Loans

- etc.

Don’t forget to pick a debt payoff strategy.

I am a huge fan of paying off debt with the Debt Snowball Method! My family was able to pay off $71,000 in less than 3 years by using a zero-based budget, driving beat-up cars with no payments, cutting back on everyone’s wants, and using the debt snowball method.

Related reading: How to Pay Off Debt Fast with the Debt Snowball Method

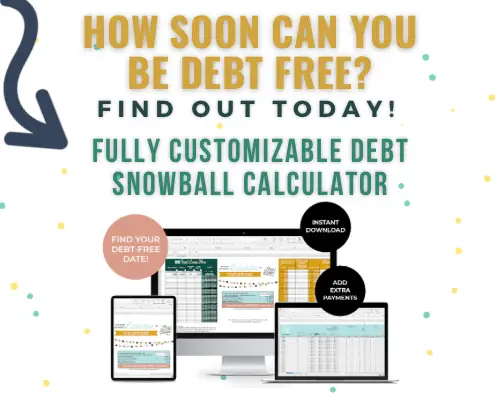

How soon can you have your debt paid off? Well, I have a really easy way to figure it out.

My Debt Snowball Calculator tool can calculate your completely customized debt-free date! Need to add extra payments in the future? No problem! Not only that, but it can operate on the Debt Snowball, Debt Avalanche, or custom order of debt payoff. There’s no guessing when you will be able to finish this step– the calculator will automatically show you.

The best part about it? The majority of people can pay off all of their debt within 2-4 years of beginning an aggressive payoff strategy!

After you identify which strategy works best for you and how long it will take, start getting used to living a more frugal way of life.

These years are all about relearning your money habits and practicing living below your means.

I’m not going to tell you that this is an easy part of the process, because it isn’t. It takes an incredible amount of control, intention and support. It takes budgeting and telling every single dollar where to go so that your income works for you and not against you.

Begin Investing for Retirement

Uh-oh… I just used the ‘I’ word. Have no fear, I’m going to make this beginning investment strategy very simple!

If you are an employee of a company that offers 401k matching, start investing 5% of your income or whatever your company match is into your 401k account. If you don’t have that option, open a Roth IRA and start investing 5% of your income into your new Roth IRA account.

Yes, you can do this step while paying off debt.

Time in the market is critical for compound interest to work its magic on your investments and grow over time.

If you can do this while still paying off your debt, that is great. If you don’t have enough money, you can start this step later on in your 5 year plan after your debt is paid off.

See? Simple.

Next, Save a Fully Funded Emergency Fund of 3-12 months of Expenses

After your debt is paid off and you’ve begun investing, it’s time to save a fully funded emergency fund. I recommend saving at least 3-12 months of living expenses in a high-yield savings account.

When determining how much to save in your emergency fund, calculate how much you’d need to live for a month (basic needs, not a lot of excess) and multiply that by 3-12 months.

Below is an example of essential bills and expenses that a family must have to survive:

- Groceries – $600.00

- Mortgage – $1,500.00

- Home Insurance – $120.00

- Water/Sewer – $62.00

- Electric – $150.00

- Home Gas – $30.00

- Cell Phones – $150.00

- Car Insurance – $119.00

- Auto Gas – $140.00

- Miscellaneous – $200.00

- Total = $3,071

Based on these numbers:

- 1 month emergency fund = $3,071

- 2 month emergency fund = $6,142

- 3 month emergency fund = $9,213

- 4 month emergency fund = $12,284

- 5 month emergency fund = $15,355

- 6 month emergency fund = $18,426

- One year emergency fund = $36,852

You may need more, this is just a very simple example. Once you have your emergency fund stashed in a high-yield savings account, it’s time to work on other savings goals!

Ramp Up Your Investing

Since you’ve been investing into your retirement accounts while paying off debt — at least 5% of your income — you are going to be building on the investing foundation that you have already started.

Once you become debt-free and have saved your fully-funded emergency fund, you’ll want to ramp up your retirement investments to a minimum of 15% of your income. The amount and where you invest really depends on your goals!

We invest primarily in real estate, but index funds are another great option. You can invest in index funds through your 401k, IRA, or a regular brokerage account.

The best resource I know of for learning how to invest properly in index funds is How to Build Wealth by Investing in Index Funds by Jeremy Schneider from Personal Finance Club. It walks you through opening an account, picking your funds and amounts, and figuring out how to automate the whole thing so you can be investing for the future and retirement.

Related reading: Clueless About How to Invest? Why Index Funds Are The Best Starting Point For Beginners

How much will you need to save each month to have ___ saved when you want to retire? Start with that question and start figuring out what those numbers will be for you. Retirement is not an age, it’s a financial number.

Note: If you’re already over the age of 35-40 when you begin your financial journey, you may want to invest 15% instead of 5% starting today, since you are closer to retirement age and it is more of a priority.

Save for Larger Expenses

Now you have the opportunity to save and pay cash for major future purchases! You get to act like Julia Roberts in Pretty Woman and pay with cash for everything!

Add sinking funds into your budget for any larger upcoming expenses you’ll need to save money for. This could be anything from a downpayment on your dream home, to braces for the kids, or a new vehicle.

Start by evaluating what you want to purchase, how much it will cost, and how much you will need to put away each month to have the amount saved by your goal date.

For example, about 4 months after becoming debt-free, we started saving for a new truck. My husband’s 2000 Honda Civic wasn’t going to last much longer! We planned to spend about $20,000 and got to work saving on it right away, about $2,000/mo plus any extra cash we could get our hands on. About 9-10 months in, we had enough cash and bought the truck.

Whatever your large future expenses are, start saving for them at this point in your journey.

Once you complete these key goals in the next 5 years, the next few decades will mostly just be maintaining. You simply have to keep up the good habits of paying for things with cash, budgeting, investing, and staying on the path to wealth!

Additional Goals to Include in Your Plan

If you already have several of these steps completed or will have them done sooner than 5 years, here are a few more options for the next steps in your financial plan:

- Increase sources of income by 1-3 (passive and active)

- Begin paying off house

- Diversify investments into things like real estate, businesses, or stocks

Set Goals for How Long Each Step Will Take You

To create your 5 year financial plan, you’ll need to write down each of these steps in the order you want to accomplish them and then estimate how long each step will take!

Then you will be able to determine how far you can get in the next 5 years and set that as your plan.

The ‘paying off debt’ step is usually the biggest and most uncertain, so don’t forget to snag my Debt Snowball Calculator to see how long this step will take you.

5 Year Financial Plan at a Glance

Let’s summarize everything we talked about above that you may want to include in your plan.

- Save a small emergency fund

- $1,000-$5,000 is perfect for a starter emergency fund

- Pay off all of your debt

- Pick a debt payoff strategy that works for you

- Debt snowball or debt avalanche

- Use my Debt Snowball Calculator to find your debt-free date and stay on top of your debt payoff journey

- Pick a debt payoff strategy that works for you

- Save a fully-funded emergency fund

- 3 months – 1 years worth of expenses

- Invest your income

- Invest your company match or 5% of your income while paying off debt

- Later, ramp up investments in your retirement accounts to at least 15% of your income

- Max out your Roth IRA or 401k contributions

- Use sinking funds to pay cash for larger purchases

- Put away money monthly to put a downpayment on a house, save up for braces, or purchase a new vehicle

5 Year Financial Plan Sample

YEAR 1: Pay off debt first 1/3 of debt, Start investing 5% of pay into 401k or IRA

YEAR 2: Pay off second 1/3 of debt, Keep investing 5% of pay

YEAR 3: Pay off third 1/3 of debt, Keep investing 5% of pay, DEBT FREE

YEAR 4: Save Emergency Fund of $20,000 (6 months of expenses)

YEAR 5: Save $18,000 for a new to us car and $5,000 for home upgrades, Increase investments to 15% of pay

Now it’s your turn! Are you ready to create your very own 5 year financial plan? Check out this FREE downloadable printable and get working on your plan today!