So you got a big chunk of money? Woohoo! Who doesn’t love a big ol’ hunk of cash? However, when you don’t have an intentional plan for big sums of money, it’s easy for it to fall right through your fingers. When you get a large sum of money from a tax refund, bonus, or something similar, you should make a responsible plan for it before you spend a dime! Let’s go over 5 things to do when you get a large sum of money so you can maximize that money and make it work for you instead of letting it slip through your fingers.

I think we all have experienced this as teens with birthday money. $100 extra one day, low rise jeans and blue eyeshadow from Justice the next. No regrets, right?

Well, as an adult with seemingly endless responsibilities– and absolutely no business wearing low rise jeans from the early 2000’s– it’s not so easy to recover from blowing money on whatever we want.

I don’t want you to have a sudden windfall, whether it’s a COVID-19 stimulus check or a bonus from work, and have the funds end up spent on stuff you didn’t need instead of getting you closer to your bigger goals.

After all, that’s the power of money — it can propel you forward or it can keep you stagnant . . . it’s all up to you!

HERE ARE 5 THINGS TO DO FIRST WHEN YOU GET A LARGE SUM OF MONEY

1. Save it into Your Emergency Fund

I know that this isn’t a necessarily “fun” thing to do with money, but with a reported unemployment rate at over 13% and millions of Americans out of work due to the Coronavirus pandemic, saving money may be the smartest move you could ever make.

I try not to operate my personal finances based on fear or lack, however, I do think it’s smart to be proactive, instead of reactionary. The worst thing that could happen is you are furloughed or laid off and you have $0 to your name with no income to support your life.

As a matter of fact, 41% of Americans can’t cover a $400 emergency. So what happens when you have to eat and pay rent when you’re out of a job?

Swiping a credit card may save you in the short term, but this will only cause more distress later down the road when you have to pay interest.

Grab my FREE Sinking Funds and Saving Tracker here

If you have average monthly expenses of $2,000 and you put $1,600 on a credit card for just one month, you can expect to pay $1,044 in interest if you pay a minimum payment of $30 per month on that balance. That is assuming no other credit card debt is in play. Let me reiterate: that’s based on just one month’s worth of expenses.

It’s a vicious cycle that is difficult to dig yourself out of once you get started– that’s why saving money is so important. Emergencies will happen.

The good news? You have the power to protect yourself with cash instead of plastic.

Related reading: Should You Keep More Than $1,000 in Your Starter Emergency Fund?

The unfortunate reality is that the world is not secure right now and our work force and the market are going through a recession. Protecting yourself and your family should be your first priority. The best way you can do that is by setting money aside in a high yield savings account for a rainy day.

2. Pay Off Debt

If you already have some money in your savings account, the next best thing you can do is pay off debt! Especially right now when so many student loan payments have been suspended by the government due to the pandemic.

If that’s you, I highly recommend throwing a chunk at Sallie Mae when she’s taking a break from interest.

If you are reading this, there’s a good chance that you are already working on your debt snowball or debt avalanche.

A windfall has the potential to drastically reduce the amount of time you spend paying off debt, getting you to wealth and financial independence faster!

With my Debt Snowball Calculator, you can tinker with the numbers in Excel or Google to find out exactly how much your large sum of money will speed up your debt payoff!!

Related reading: How We Paid Off $71k of Debt in Less Than 3 Years on a Single Income

Paying off debt is never a bad id . . . especially when the average numbers look like this:

| Debt Type | Average Amount Borrowed |

| Student Loan Debt | $35,397 |

| Credit Card Debt | $5,700 |

| Auto Loan Debt (new) | $32,480 |

| Auto Loan Debt (used) | $20,446 |

This chart doesn’t include personal loans, mortgages, or medical debt, but I think you get the drift: Americans have a debt problem and a windfall of money can help you get out of that problem quicker!

3. Save it For an Upcoming Expense

Sinking funds are the way that most financially independent people are able to afford things with cash instead of going into debt for them.

Simply put, sinking funds are where you save an allotted amount of money per month into a single fund for a set amount of time to save up for something specific.

At the end of that time period, you will have saved the total amount of money you need. This way, you aren’t slammed with needing $1,000 all at once in December for Christmas– you’ve saved up $100 for 10 months and you have your money ready to go! No mess, no stress!

As you can imagine, an unexpected amount of money can build up sinking funds quicker and relieve stress in other areas of your life. If you get $1,000 and you put it into your Christmas sinking fund instead of spending it, that frees up $100 per month to put towards debt, savings, another sinking fund, or even in your ‘fun’ budget!

4. Invest

Let’s say your Emergency Fund is looking great, you have paid off all of your debt and putting the money into a sinking fund doesn’t really interest you because you’re one of those people that like to just stick to a monthly plan.

First of all: Wow! Congratulations! You are well on your way to building a financially independent life and nothing makes me happier than that!

Second of all: This is your time to shine, my friend. With a windfall of cash you get the choice to invest this money and make it make more money for you! Huzzah!

Grab my FREE Net Worth Tracker here

If you are in this boat, I recommend maxing out your retirement accounts, tax-advantaged accounts, or investing in other areas of your investment portfolios.

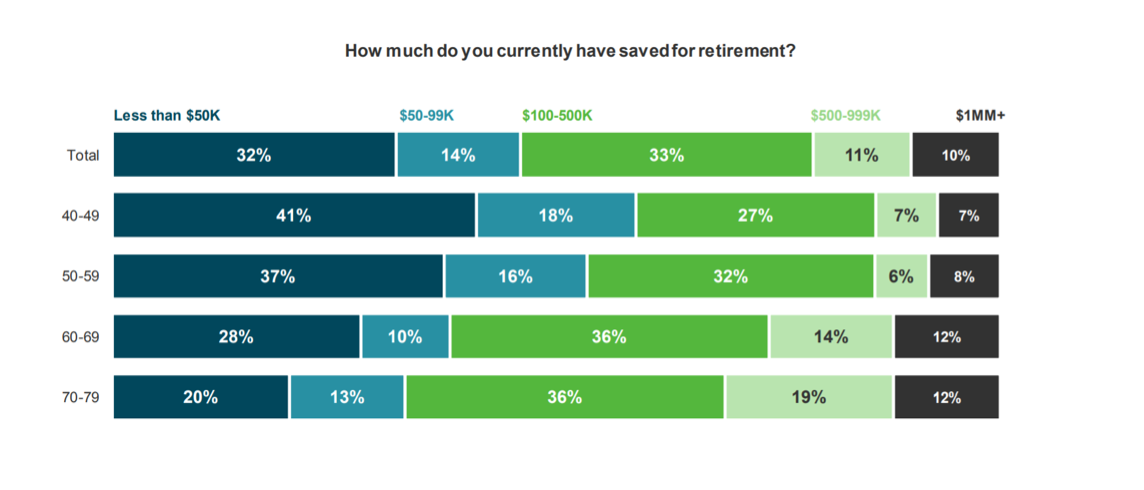

I know retirement isn’t exciting to talk about; however, it is inevitable that you are going to age and need money. Unfortunately ⅔ of 40 somethings have less than $100,000 saved for their golden years.

Yikes.

Build up your net worth through index funds and retirement contributions, because that’s how you really win with money and take care of yourself later in your life.

5. Spend it on an Important Family Need

Is there something happening in your family that will be costly? It would be a good idea to spend the money on it so you don’t end up putting that expense on a credit card. Some examples would be braces, plane tickets to visit family, or a new roof. All these items are important or essential and would be a wise way to spend your big chunk of cash sooner rather than later.

Bonus: Mix ‘n Match

The last, but certainly not least, is to mix and match these ideas! Who says you have to stick to one thing when you get a bug chunk of money? That’s right, absolutely no one!

Personal finance is personal, and that’s the great thing about it– you get to decide how you make your money work for you!

Depending on the size of the money you receive, mixing saving, debt payoff and investing may be the smartest choice you could make.

I also want to point out that it’s entirely healthy to spend money on yourself. I’m not saying go out and spend the entire amount on frivolous things, but I am saying you have to find balance, and treating yourself is a good thing. It prevents budget resentment and debt payoff burnout. Trust me!

If you’re going to go this route, split your windall in half or into thirds and use the money in different areas of your financial life that need attention.

Windfalls can be a wonderful way forward in your financial journey, as long as you know what to do when you experience one. These guidelines will help you decide how to use them in a smart way!

Would you use a large sum of money on one of these 5 things first? Let me know in the comments below!

Did you enjoy this post about what to do when you get a large sum of money? Pin it to Pinterest for later!

One Response

Yes it was helpful and debt first then investing and saving