When it comes to Dave Ramsey, are you a loyal follower or a total rebel? Either way, it’s important to know that Dave Ramsey gives some amazing advice on money, but he also gives some advice that could actually make you poorer!

Today, we will analyze his advice for errors and discuss solutions that create optimal wealth building.

Dave’s advice about paying off debt is revolutionary and helping so many families take the next step toward financial freedom. That’s why most of Dave’s bad advice is related to saving and investing.

Investing can be intimidating. There are words that are difficult to understand, processes that seem complex, and a lot of conflicting advice out there. Dave really simplifies his investing advice to work for the masses. Because of that, some of Dave Ramsey’s advice is good for people who are bad with money, but bad for people who are good with money.

“Some of Dave Ramsey’s advice is good for people who are bad with money, but bad for people who are good with money.”

Today I’ll be breaking down 3 pieces of Dave Ramsey investing advice. I go through each recommendation with Dave Ramsey’s take, how it can negatively affect your finances, and what I recommend doing instead.

I hope you will use this information to make an informed decision for your family and your personal finance journey that will best serve your money needs now and in the future!

Here are 3 Pieces of Dave Ramsey Advice that Will Actually Make you Poorer (and what to do instead):

1. Cancelling 401k Contributions During Debt Payoff

What Dave Ramsey recommends: Dave recommends not investing in your retirement accounts while paying off debt. The idea is that, instead of investing, you use all of your “fire power,” aka: your income, on debt. This will speed up the debt payoff process and free up more money to invest once you are debt-free, a bit down the road.

Why it can make you poorer: If you have a 401k retirement account that offers employee matching, you can lose out on free money from your employer! You will also lose out on those critical early years of compound interest where your money is beginning to grow.

For example, if you make $40,000/year and invest 4% of your paycheck to the amount of $1,600/year, your company will put $1,600 of free money into your 401k account to match it. That’s $3,200 a year that you’re investing – and only paying for only half of it!

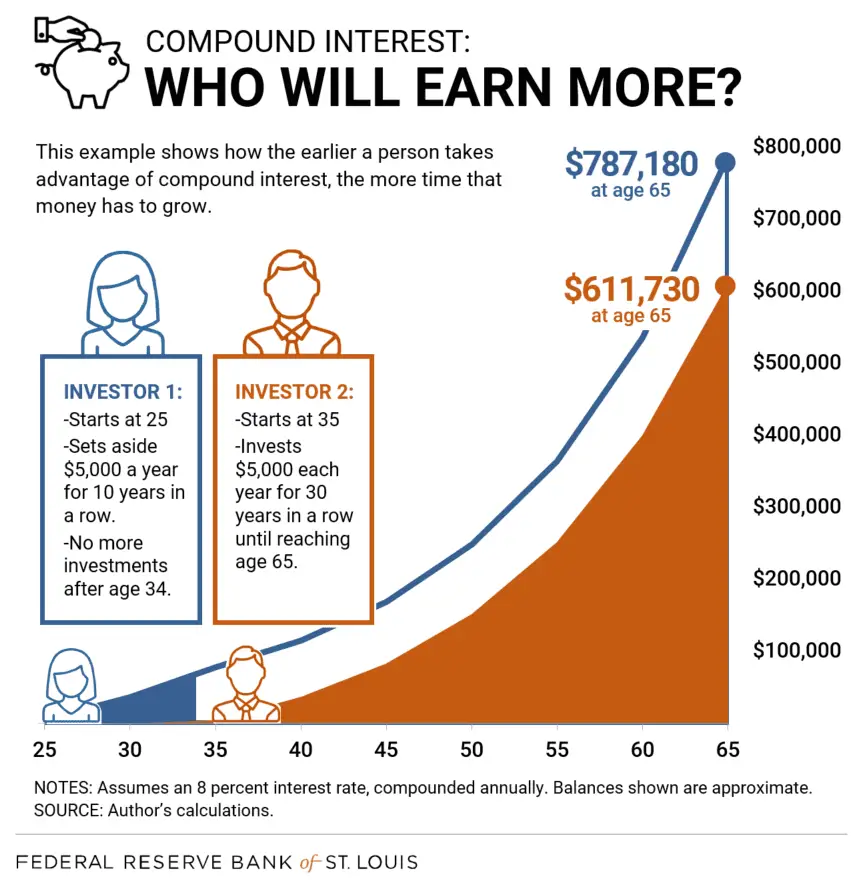

Not only could you lose money via company matching, but you will also lose out on compound interest time in the market! The earlier a person takes advantage of compound interest, the more time that money has to grow, and the results are significant.

Notice how investor 1 started 10 years earlier than investor 2, stopped contributing at age 34, and still became wealthier! That’s the power of compound interest early on!

While every 401k account is different, the average return ranges somewhere between 5%-8%.

Taking from our example before, if you invest $1,600 in your 401k and your company fully matches that 4% contribution each year, you could make $128 off of interest in one year!

| Year 1 | Year 2 | Year 3 | Year 4 | |

| Personal 401K Contribution | $1,600 | $1,600 | $1,600 | $1,600 |

| Company Match | $1,600 | $1,600 | $1,600 | $1,600 |

| Interest | $128.00 | $394.24 | $681.78 | $992.32 |

| Total: | $3,328 | $6,922.24 | $10,804.02 | $14,996.34 |

That means that after four years, you could have nearly $15,000 in your 401k, when you only put in $6,400. This is without the average 3% yearly raise, and based off of an average return of 8%.

That’s the power of compound interest!

Please note, that the annual rate of return and interest earned on your retirement accounts will fluctuate with the current market environment. There are multiple online calculators you can mess around with to test out different situations and variables. This is the one I used for the chart above.

What to do instead: Keep investing into your 401k if you can afford to while paying off debt! If money is so tight that your 401k contribution cash is the only money you have to put toward debt, then it’s not a bad idea to postpone retirement savings to get the debt squared away. As long as it’s quick.

2. Investing 15% Into Mutual Funds Until Retirement

What Dave Ramsey recommends: Dave recommends that after you pay off all of your debt, excluding your home, you should invest 15% of your income into mutual funds. He recommends 4 different types of mutual funds: Growth and Income, Growth, Aggressive Growth, and International. These different mutual funds allow you to diversify your portfolio. In other words, you’re not putting all your investing eggs in one basket.

Why it can make you poorer: Once you pay off your debt and save your fully-funded emergency fund, you’ll more than likely want to focus even more aggressively on retirement and even retiring early. Investing just 15% of your total income into 4 types of mutual funds will not allow most to retire earlier than 65. Further, mutual funds (especially the ones Dave recommends through his ELPs) are usually high-fee accounts. The fees they charge to manage your accounts seem small, but that’s their trick. They can actually cost you thousands of dollars in fees and hundreds of thousands of dollars in foregone compound interest earnings.

What to do instead: Try out a customized investing strategy that works for you. There are many books out there that I recommend on investing. Here are my top 3:

- Broke Millennial Takes On Investing by Erin Lowry

- Smart Couples Finish Rich by David Bach

- The Simple Path To Wealth by JL Collins

You may also consider managing your own investments and avoiding high-fee mutual funds, which can skim off your earnings significantly. Index funds can be much better than mutual funds if you manage them well. I recommend focusing on investments with low fees like index funds and real estate. Avoid mutual funds with huge fees.

| Mutual Fund Fees | Index Fund Fees |

| 0.5-1.0% | 0.04-0.09% |

| $2,500-$5,000/year on $500k portfolio | $200-$450/year on $500k portfolio |

You may be thinking that the difference between $450 a year and $5,000 a year in fees isn’t too bad. However, you must also consider how the money you spend on fees is not earning you interest anymore and you are losing out majorly on compound interest!

Let’s say you are age 40 and your portfolio is $500k. The $4,550 difference in cost between a high fee mutual fund and low-cost index fund, if you kept it in your investment account each year for 20 years until you were age 60 and it grew at 8% compounded annually, would be $246,000.

Yes, you read that right! $246,000 in foregone dollars because of high fees in your portfolio.

The main reason to choose a mutual fund is if you don’t have time to manage your own investments or you think your mutual fund will outperform the market. If you find one, make sure it’s as low fee as possible, because as you can see, those fees could cost you big time.

You should be keeping track of your wealth and preparedness for retirement via your Net Worth. If you don’t know your Net Worth yet, start tracking it for FREE here: Personal Capital

3. Keeping Your Emergency Fund in a Money Market Account

What Dave Ramsey recommends: Dave recommends putting your emergency fund, both your starter emergency fund ($1,000) and your fully-funded emergency fund (3-6 months worth of expenses) in a money market account (basically just a regular savings account). This is because your “Emergency fund is not an investment…” While I agree that your emergency fund is absolutely not an investment and you shouldn’t place it in a retirement account or illiquid investment, keeping it in a money market account could actually make you poorer.

Why it can make you poorer: Traditionally, a money market account has an average national return of 0.18%. That rate is for deposits under $100,000. If you have more than that in your account, you make an average APY of 0.29%. Both of these are much lower than you could be earning! By putting your emergency fund in an easily accessible high yield savings account, like Ally or Capital One 360, you can make from 0.80%-2.25% on your money just sitting in an account.

| Starter EF ($1k) at 0.18% APY | 6 Month EF ($10k) at 0.18% APY |

| $1.80 End of Year (when compounded daily) | $18.02 End of Year (when compounded daily) |

| Starter EF ($1k) at 0.80% APY | 6 Month EF ($10k) at 0.80% APY |

| $8.03 End of Year (when compounded daily) | $80.32 End of Year (when compounded daily) |

Will this make you rich? No. However, by making high compounding interest a habit in your personal finances, you are using a wealth mindset and finance technique that will absolutely make you poorer if you don’t take advantage of it.

What to do instead: Place your emergency funds in a high yield savings account. Typically these accounts are online banks and offer higher returns than a money market account. Make sure they are FDIC approved and that you aren’t going to be hit with any service fees. You can check out my top 5 high yield savings account options here.

Personal finance is personal and making decisions that work for your specific money situation and family is more important than just about anything.

Dave Ramsey and his advice have touched so many people and helped them get out of debt and begin thinking about their financial future, freedom and independence. However, his financial advice is simply an exciting starting point for your own educational journey into all things personal finance and investing related!

Using his advice and your own knowledge and expertise, you can craft a customized plan for your finances that will make you wealthier.

Take a critical approach and make the best decisions for you and your family, especially when it comes to investing advice!

Did you find these 3 pieces of Dave Ramsey advice that could actually make you poorer helpful?

Did you enjoy this post about 3 Pieces of Dave Ramsey Advice that could actually make you poorer? Save it to Pinterest for later!

7 Responses

Merilee, I so appreciate what you have done here. I have long expected that to follow Dave Ramsey’s advice to a tee is likely no better than kicking it all to the curb. Thanks for the breakdown on the weak spots in his financial guidance. I know A LOT less than you do on money matters but am grateful that you put things into terms I can understand. I’m starting my own business at MyNameIsElizabethAnne.com and JourneyToAJog.com and am looking to pay off long standing debts in the coming year. I’ve got your site bookmarked as a place I will want to return to often.

Contributions to your employees’ accounts may be a tax-deductible business expense.

Merilee Speigner, are you a multi-millionaire yourself like Dave Ramsey? He helps thousands of people about their financial situation for years. He has a show and answers phone calls with all kinds questions about money. Do you ? Why should people think you are better? Do you have debts? Maybe you should call his show and tell him that his financial advise will make people poorer. It appears that you are just one of those financial gurus who thinks they’re financially smarter.

I believe there is nuance to personal finance, and notice how I didn’t say Dave Ramsey sucks and you shouldn’t listen to anything he says? I don’t feel that way. He helps a lot of people on their journey’s, including us, but in this article I want to stretch the thinking a little bit and get people thinking for themselves on a few issues. Not every piece of advice he gives is the best, I know that for sure. Good luck!

Ramsey advice will allow retirement at 60 or even 58. Can’t argue with any of it!

Dave has always said to put your emergency fund in a high yield savings account. Please check your facts before spouting fallacies just for a blogpost’s sake. This article is also misleading in point number 1 when you say Dave tells you to stop retirement contributions during debt payoff. He tells you to pause them during consumer debt payoff, not mortgage type debt. The recommendation is to pause them for maybe a year or so tops while you clean up consumer debt. You lead the reader to believe (intentionally I think) that he tells people not to contribute for a LONG span of time, like maybe a 10 year period. That’s simply not true. You have ok advice too, just don’t smear the other guy when you really aren’t familiar with his system.

I’m extremely familiar with his system! I followed it for 2-3 years! This article was also written in 2020 so I think a few things have changed since I wrote it. I just checked his website and for storing your Emergency Fund he does recommend a regular savings account, money market account, or a high yield savings account – so that is great. I think that’s good advice (I need to update my article). However, on the investing while paying off debt and choosing highly managed mutual funds instead of simple self-managed index funds, I stand by my original stance. I don’t think I made it sound like Dave recommends to NOT invest while paying off the mortgage or anything long like that. But many people’s debt payoff journey take 4-5 years and if they’re in their 30s, 40s, and 50s… I don’t recommend they stop investing, especially if they get any kind of company match! I absolutely appreciate your thoughts and will update this article!